VOLATILITY IS ALWAYS STRESSFUL

With lingering concerns about trade, markets sold off Monday with all three major U.S. indexes posting intraday declines of greater than 1%. Red screens create stress and doubt. Therefore, it can be helpful to take a step back and check the big picture.

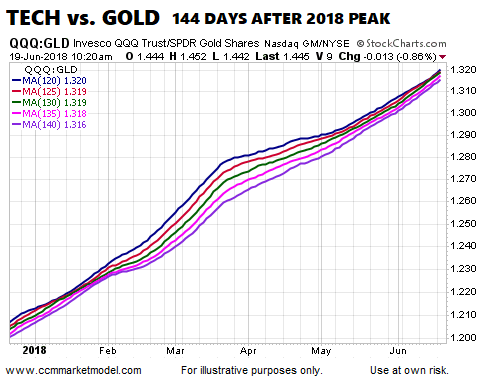

In August 2016, the S&P 500's 30, 40, and 50 week moving averages told us to be open to better than expected outcomes from a long-term perspective. The chart below shows the same moving averages as of 1:15 pm ET Monday. The NASDAQ's chart looks even better.

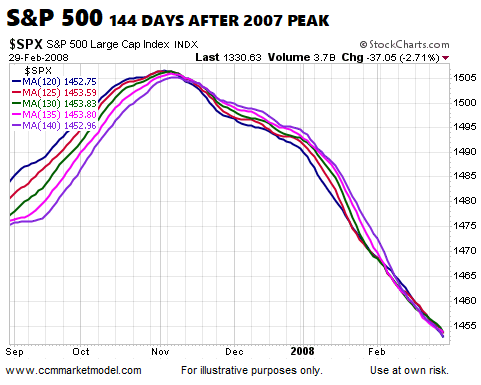

To give us a bearish reference point, the same weekly moving averages over a one-year period in 2007-08 are shown below.

The daily chart below shows the S&P 500's 200-day moving average as of 1:28 pm ET Monday. The NASDAQ's 200-day paints a similar picture.

To give us a bearish reference point, below is the same 200-day moving average over a one-year period in 2007-08.

SOME HISTORICAL PERSPECTIVE

In May 2003, stocks had made little progress YTD. Despite numerous swings up and down into year-end, the S&P 500 finished with a very satisfying gain of 26.38%. Day-to-day volatility provided little in the way of useful information between points A and B.

2004 featured numerous bouts of stress-inducing volatility, including the S&P 500 moving into negative territory YTD numerous times. Patient investors were rewarded with a gain of almost 9%. Even in the context of a longer-term bullish trend, volatility is to be expected.

Trying to trade between point A and point B in 2005 proved to be a difficult task. When the volatility dust settled at the end of the year, the S&P 500 managed to post a positive gain.

2006 featured several moves above and below the S&P 500's 200-day moving average, along with a push into negative YTD territory as late as July. Once the summer doldrums passed, stocks rallied hard into year-end providing patient investors with a satisfying gain of 13.62%.

NASDAQ: BUBBLE OR OPPORTUNITY?

This week's video takes a very long-term view of the NASDAQ using quarterly charts, allowing us to address the following question:

Does the NASDAQ look more like a bubble that is about to pop or a long-term opportunity for investors?

RESPECTING CONCERNS ABOUT TRADE

Based on the facts in hand today, the market's longer-term trend remains constructive. With ongoing uncertainty related to the economic impact of trade tensions, it is important we continue to review the data day-by-day with a flexible, unbiased, and open mind.